Worldwide Smartphone Shipments to Grow 7% in Q4, Says IDC

NEEDHAM, MA – Worldwide smartphone shipments are forecast to see 7.3% year-over-year growth in the fourth quarter, according to IDC's Worldwide Quarterly Mobile Phone Tracker.

The improved forecast for the holiday quarter follows the modest improvement in the third quarter without further inventory buildup, which has led some channels and major OEMs to ramp up their business plans for the months ahead. The market recovery will continue in 2024 with 3.8% growth expected, followed by low single-digit growth for the rest of the forecast period, resulting in a five-year compound annual growth rate of 1.4%.

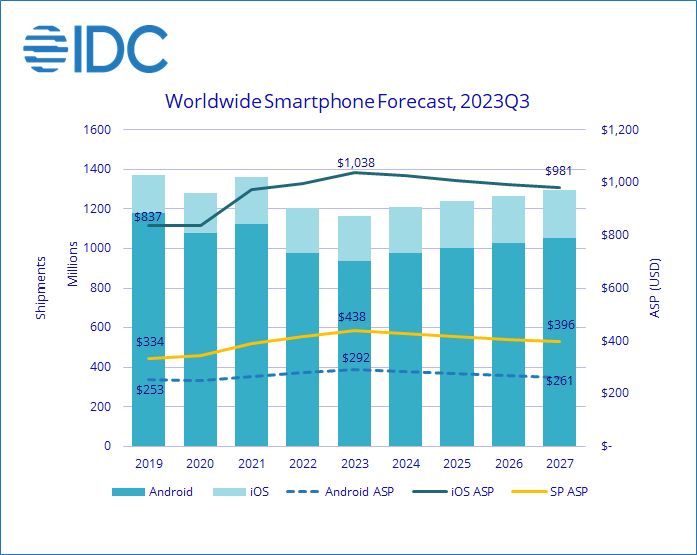

Despite improved expectations for the fourth quarter, worldwide smartphone shipments are forecast to decline 3.5% year over year in 2023 to 1.16 billion units. The revised forecast for 2023 is an improvement over the decline of 4.7% forecast earlier in the year.

"The tide has finally turned and it feels safe to say the worst is behind us," said Nabila Popal, research director with IDC's Mobility and Consumer Device Trackers. "While the rate of recovery varies across regions, the changed sentiment is most apparent in China, where consumers are finally coming out of their shells and spending on devices, fueled by the excitement from Huawei's resurgence, which is in turn expected to have a positive impact on the larger Android market in the long-term. More importantly, as we enter the new era of low single-digit growth and lengthened refresh cycles, it is clear the market is maturing. While the total available market will remain below pre-pandemic shipment levels throughout the forecast, the bright side is that average selling prices (ASPs) and market value will remain notably higher than before."

Smartphone ASP is expected to rise 5.5% in 2023 to $438, marking a fourth consecutive year of growth as the premium market continues to grow across all regions. However, ASP growth is expected to taper off and gradually decline to $396 by 2027, which remains higher than prior forecasts. From an operating systems (OS) perspective, iOS remains more resilient to macro challenges with 0.6% growth, achieving a record share of 19.6% this year, while Android is forecast to decline 4.4%. Over the long term, Android will grow slightly faster than iOS, increasing its share of the market to 81.3% by the end of the forecast period.

"Despite another lackluster year for smartphones, 5G adoption continues to be a bright spot in the overall market," said Anthony Scarsella, research director with IDC's Worldwide Quarterly Mobile Phone Tracker. "With 5G devices becoming less relevant in most developed markets, the growth of 5G in emerging markets will play a crucial part in the rebound next year and throughout the forecast period. Global 5G shipments are expected to grow 11% in 2023 and 20% in 2024. Moreover, the share of 5G smartphones will jump from 61% in 2023 to 83% by 2027. While the smartphone will witness a small 1.4% CAGR from 2022-2027, 5G shipments will demonstrate an impressive 11.1% growth rate for the same period."